Too Many Credit Cards May Affect Mortgage

Having credit cards for the benefit of signup bonuses may affect the amount of mortgage the bank would approve you for.

Of course if you just cancel the CCs after you have received the bonuses (don’t know how long for you need to own the CC in order to keep the bonus, I wasn’t interested at all in accumulating credit cards) I would think it should not matter for the mortgage approval. Or even better if you don’t need any mortgage at all I suppose you can have as many CCs as you wish if there is no annual fee, that’s it :).

I ‘dicovered’ this while I was looking for a mortgage and I came across this page ‘How Much Home Can I Afford?’.

It is for a Canadian bank but I have a feeling the US banks work the same (at least now after they have been burned badly with the subprime).

So keeping all the other information the same I played with the credit cards:

and the result

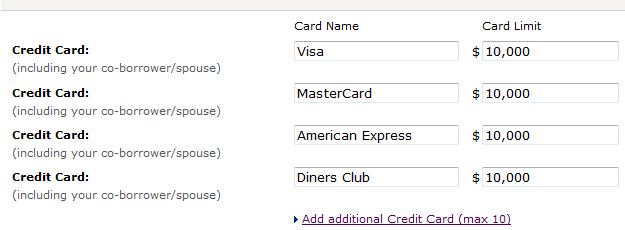

Now let’s add a few more credit cards.

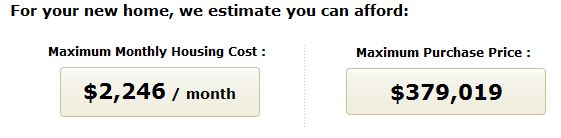

and the result:

That’s a huge drop from $500K to $379K.

However, let’s suppose you have one main credit card with a limit of $10,000 and two other CCs with a limit of $5,000 each.

Now it is much better.

For the sake of it let’s assume you don’t own any credit card.

It does not make any difference.

I have played around with other combinations

1 Credit Card – 10K limit + 1 Credit Card – 5K limit: $500K maximum purchase price (same as no CC or 1 CC with a 10k limit)

1 CC-10K + 1 CC – 7K: $492K max.

1 CC – 10K + 1 CC – 10K: $477K max.

1 CC – 10K + 1CC – 5K + 1CC – 3k: $487K max.

1 CC – 10K+ 1CC – 5K + 1CC – 5K: $477K max

So owning too many credit cards may affect the mortgage you can get. Of course, this is only an online tool and more complex calculations are involved when the bank really determines how much they can approve you for.

Don’t these type of calculators assume when you put $10,000 for each credit card is the actual balance you are carrying? Thus reducing your ability to service debt. It’s not the actual number of cards or the total available credit that matters. It is ratio of blance to avilable credit (total credit lines) that hits you if it is too high. Zero blance–zero hit to your ability to borrow.

This is not true in the US — at least not directly. As long as your credit score is sufficient, banks look at DTI, not # of credit cards or credit limits.

From what I have read, the more credit you have, the lower your score. This can be cancelled out in part by a lower credit utilization ratio, but it certainly doesn’t help your score to have more than a few credit cards.

Funny..I actually was just speaking with a home loan finance specialist with Bank of America earlier last week about home loans and credit. She said that the number of credit cards I have doesn’t affect my home loan qualifications, so long as my credit score is excellent and I never miss a payment on any of the cards. Certain other factors (i.e. whether or not you are carrying over balances and how much total credit you are utilizing) will also affect the loan, but she said that the total number of cards or total credit limit didn’t affect it.

That being said, what I got out of my conversation with her was that the biggest thing that banks look at for pre-qualifying home loans is how much total debt you have (student loans, car loans, credit card debt, etc.), your credit history (if there are any late payments, etc.), and then your total income (after expenses).

So I guess that in Canada it might be different? (This was a Bank of America home loan specialist in California btw, so maybe it’s also different by state.)

I agree with both of the above (or perhaps the estimator is broken.) 40k of credit limit is pretty small if you have the income to be approved for a 500k mortgage. Unless typical limits are much lower in Canada?

In the U.S., having no cards (along with no history) will surely impact your mortgage. At least in the typical case, no CCs usually means a lower credit score, which likely means a higher mortgage rate. That would impact the amount of the loan allowed because the higher rate would require a smaller principle to generate the same monthly payment. Though it wouldn’t be anything like the 25% shown in the 40k example.

Also, having a very low combined credit limit is more likely to result in a higher credit utilization, which would also negatively impact the mortgage offered.

Of course, as you point out, Canadian banks didn’t screw the pooch like ours did. Maybe, *just maybe*, rewarding people for having rediculous credit limits isn’t the way to go… 🙂

Thank you for all the comments! It is clearer now for me and for any readers who might stumble upon this post.

I would have thought that the more CCs you have the lower the amount for mortgage that you can be approved for is and the estimator confirmed my assumptions.

I mean you might go on a shopping spree and CCs payments will take priority over the mortgage payments due to the higher charges.

However, the banks might reason that if you have been responsible until now you just won’t do the above and CCs should not matter.